This briefing examines international students in the UK. It presents statistics on their numbers, characteristics, economic impact, what they do after their studies, and how many settle in the UK.

-

Key Points

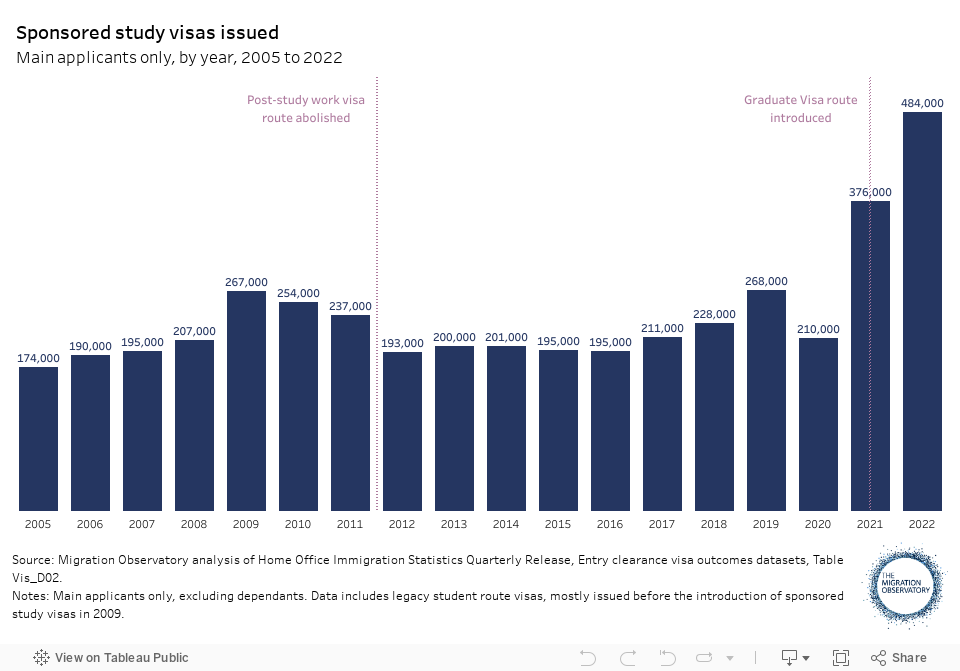

- Student migration to the UK reached an all-time high in 2022, as more than 484,000 visas were issued

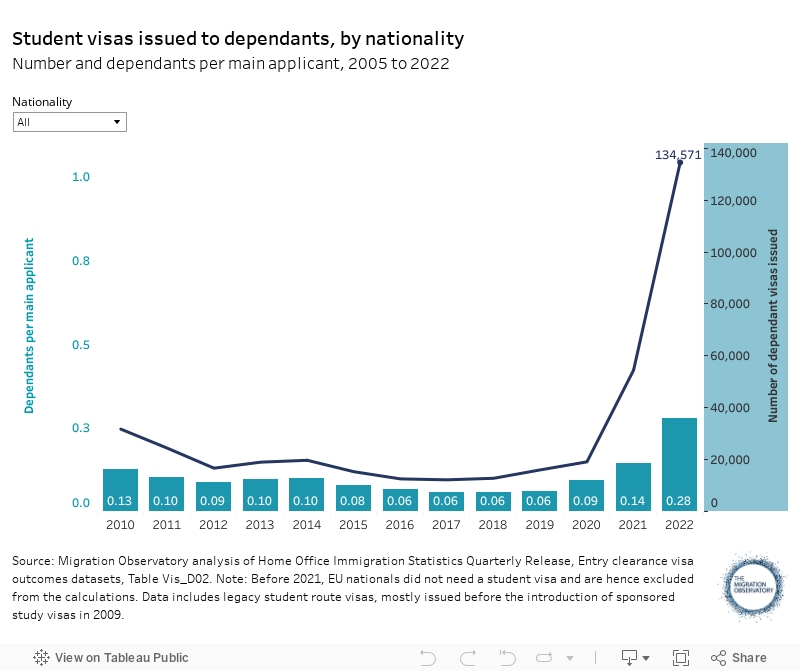

More… - About 134,000 visas were issued to student dependants in 2022, eight times more than in 2019

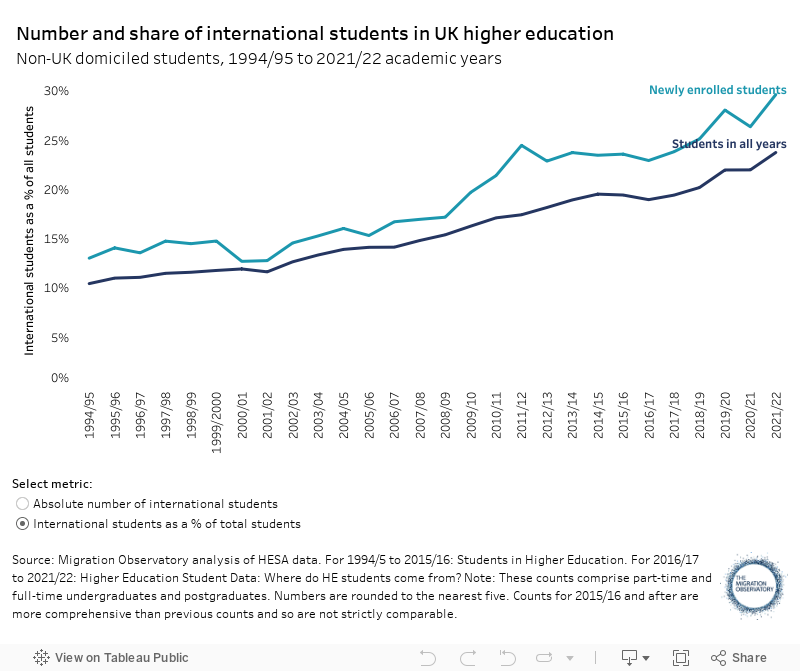

More… - In the 2021/22 academic year, approximately 680,000 international students were enrolled in UK higher education, making up 24% of all HE students

More… - New student enrolments from the EU fell by 53% in the 2021/22 academic year, the first under post-Brexit rules

More… - In 2021/22, the top countries of origin for international students in the UK were China (26%), India (23%), and Nigeria (9%)

More… - For the eighth year running, University College London received the largest number of new international students

More… - The UK recovered its position as the second most popular destination in the world for international students in 2021

More… - A record number of former students – almost 73,000 – extended their visas in 2022 through the new Graduate route

More… - In the past, most non-EU students left the UK after their studies

More… - Students who remain in the UK usually take ten years to settle

More… - In 2021/22, more than a fifth of British universities’ total income came from the tuition fees of international students

More… - Research has consistently found that international students have a positive economic impact in the UK

More…

- Student migration to the UK reached an all-time high in 2022, as more than 484,000 visas were issued

-

Understanding the Policy

Under freedom of movement, EU citizens paid the same tuition fees as ‘Home’ students, and were entitled to the same taxpayer-subsidised tuition fee loans. This meant that they did not have to pay any money upfront for tuition fees. ... Click to read more.However, following the end of free movement on 31 December 2020, the academic year 2020/21 was the last year that EU citizens enjoyed the same benefits as Home students. From 1 August 2021, new EU students have generally been subject to higher international student tuition fees, without entitlement to government-subsidised loans. From 1 January 2021, all foreign citizens require a visa to come to the UK to study for more than six months (and some require visas to study for less than six months). Because EU citizens now have to apply for a student visa, they bear a substantially higher financial and administrative burden than under free movement.

In this briefing, we use the term ‘EU’ citizens to refer to those who enjoyed free movement rights before 2021. Note, however, that this also includes non-EU citizens with free movement rights, namely citizens of Switzerland and the EEA countries Iceland, Lichtenstein, and Norway. ‘Home’ students refer to British and Irish citizens who ordinarily reside in the UK and have lived there for at least three years before starting their course.

Non-UK nationals can apply for a visa to study with an approved education provider, as long as they meet minimum English language requirements and can support themselves while they are in the UK. The Student route in the post-Brexit immigration system is largely unchanged from the one it replaced, which was known as ‘Tier 4’, and was a part of the previous five-tier system.

In recent years, there have been several changes to international student policy. In 2008, the post-study work route was expanded to allow students of any subject to stay in the UK for two years after graduation and work in any job, without needing to be sponsored by an employer. This route was closed to new applicants in 2012, and students’ permission to work was restricted. However, this route was reintroduced on 1 July 2021. Rebranded as the ‘Graduate visa’, it allows students to stay in the UK for two years after graduation – or three years if they are a PhD graduate – to live and work at any skill level, and to switch into skilled work routes if they find a suitable job. Applicants must pay the Immigration Health Surcharge, which is currently set at £624 for each year the person will be in the UK and must be paid upfront, along with the visa application fee, which was £822 as of November 2023.

When international students apply to continue their stay in the UK on a Skilled Worker visa, their employers do not have to pay them at the ‘experienced worker’ rate, but rather a 30% lower salary for ‘new entrants’, although that salary must be at least £20,960.

In 2019, the UK government published a policy paper on its International Education Strategy (with the latest update published in 2023). The paper set targets to increase the value of education exports to £35 billion per year, and the number of international students hosted in the UK to at least 600,000 per year by 2030. The latter of these targets has already been met (see Figure 2).

In response to a rise in student dependants, the government announced a change of policy in May 2023. Until January 2024, all international postgraduate students were eligible to bring their partner or children to the UK as dependants. From January 2024, this right will be restricted to international students on postgraduate research programmes, which make up about 5% of the total.

-

Understanding the Evidence

Many international students stay in the UK for only a few weeks to study English (see reference below). ... Click to read more.This briefing is concerned with longer-term international student migration, with a focus on further education and higher education, rather than students in other educational institutions such as vocational colleges or English language schools. Higher education institutions are recognised bodies with the power to award degrees and include all UK universities.

In this briefing, most data on international students in UK higher education come from the Higher Education Statistics Agency (HESA). HESA categorises students by ‘domicile’: a person’s place of permanent residence before they started their course. This means that some non-UK nationals are UK-domiciled students, and some UK nationals are domiciled overseas. Data are sometimes restricted to “newly enrolled” students, to give an indication of annual inflow. In 2021, HESA changed its data to make it more comprehensive. This means that statistics after 2021 are not strictly comparable with those for previous years.

This briefing also uses Home Office administrative data on student visa issuances and extensions. Before 2021, these data did not include EU citizens, who before 2021 did not require visas. For 2021, these data are for both EU and non-EU citizens. Visa data are thus only comparable before and after 2021 if EU citizens are excluded.

Analysis in this briefing of the UK’s global market share of students is based on data from UNESCO. These data concern ‘tertiary students’, which comprises students at ISCED levels 5 (short-cycle tertiary education), 6 (Bachelor’s or equivalent level), 7 (master’s or equivalent level), and 8 (doctoral or equivalent level).

Information on the settlement of students comes from Home Office data on the visa status of non-EU migrants over time, known as ‘Migrant Journey’ data. These data provide the immigration status of an annual cohort of new non-EU-citizen entrants at the end of each calendar year after their arrival, and may be used to calculate the share of those entering the UK on a student visa in a given year who have settlement or citizenship, or permission to stay in the UK on another visa, five years later. Note that the data show only whether the person is still authorised to live in the UK, and not whether they are actually still here.

Student migration to the UK reached an all-time high in 2022, with around 484,000 study visas issued

Student migration to the UK reached a record high in 2022. Around 484,000 sponsored study visas were issued, which are for university or college students and exclude short-term study visas – 38% more than were issued in 2021. (Figure 1). Student migration rose sharply after the COVID-19 pandemic, which caused a temporary fall in the number of international students arriving in the UK.

Figure 1

Several factors likely contributed to the sharp rise in student migration after the pandemic. First, government policy was explicitly aimed at increasing student migration. The International Education Strategy, first published in 2019, set a goal of increasing the number of international students to 600,000 a year by 2030, which was achieved in 2021. Additionally, the government introduced the Graduate Visa route in 2021, allowing students to live and work in the UK for two years after graduation, or three years for PhD graduates. This is likely to have increased the appeal of the UK as a destination for international students, although it is important to note that student numbers were already rising fast before the Graduate route was announced.

Second, as discussed later in this briefing, UK universities face strong financial incentives to attract more international students. An increasing proportion of universities’ income comes from international students’ tuition fees, which are significantly higher than the ones paid by domestic students. Additionally, the UK may have become a more appealing destination for international students during and immediately after the pandemic. Other top destinations, including the US, Canada, and Australia, implemented strict restrictions on entry and visas, resulting in long delays and higher denial rates. In comparison, the UK remained relatively accessible to international students, which may have increased its appeal.

Around 134,000 visas were issued to student dependants in 2022, eight times more than in 2019

In 2022, over 134,000 visas were issued to student dependants, an all-time high, and eight times more than the roughly 16,000 issued in 2019 (Figure 2). Until January 2024, all postgraduate students could bring partners or children as dependants. From January 2024, this is no longer permitted unless a person is on a research course (in most cases, a PhD).

A combination of two factors drove the increase in dependants when they were still permitted. First, there were more international students. In particular, the number of international students enrolling on a new postgraduate course rose by 41% between the 2019/20 and 2021/22 academic years (Figure 4). Second, students brought more dependants with them during the same period – from an average of less than 0.1 dependants per student in 2019 to about 0.28 in 2022 (Figure 2).

To a large extent, the increase in dependants was linked to higher student migration from India and Nigeria. Nationals of these two countries made up almost three-quarters (74%) of dependant study visas issued in 2022 – 60,200 were issued to Nigerians (45%) and 38,800 to Indians (29%). Students from Nigeria were much more likely to bring dependants with them than other top nationalities, with an average of more than one dependant (1.02) per student in 2022. In contrast, Indian students brought an average of 0.28 dependants per student, while American and Chinese students brought almost no dependants (0.01 and 0.07 dependants per student, respectively).

Figure 2

In response to the rising number of dependants, the government announced in May 2023 that it would restrict the right of master’s students to bring their partners or children. The impact this restriction will have on the number of dependants in the future is unclear. In the 2021/22 academic year, 95% of new international postgraduate students (252,000 of 267,000) were on taught courses and would no longer be eligible to bring dependants. The Migration Advisory Committee estimated that the ban on students’ family members might reduce long-term immigration by between 90,000 and 120,000, and net migration by anywhere from 20,000 to 50,000.

In the 2021/22 academic year, approximately 680,000 international students were enrolled in UK higher education, making up 24% of all HE students

In the 2021/22 academic year, around 680,000 international students were studying in UK higher education institutions, the largest number on record. For the second year in a row, the figure exceeded the target of 600,000 by 2030 set in the government’s Higher Education Strategy (Figure 3). Since the 1990s, the share of international students in the UK has steadily increased. In 2021/22, they comprised 24% of all students in UK higher education, compared to 17% in 2011/12 and just 12% in 2001/02.

Despite a fall in student visa issuances during the pandemic, the number of international students continued to grow. One likely explanation for this inconsistency is that people enrolled at UK universities but studied remotely and therefore did not require a visa to enter the UK. Analysts have also argued that the pandemic increased the demand for higher education by making the alternatives – underemployment or unemployment during a recession – less attractive.

Figure 3

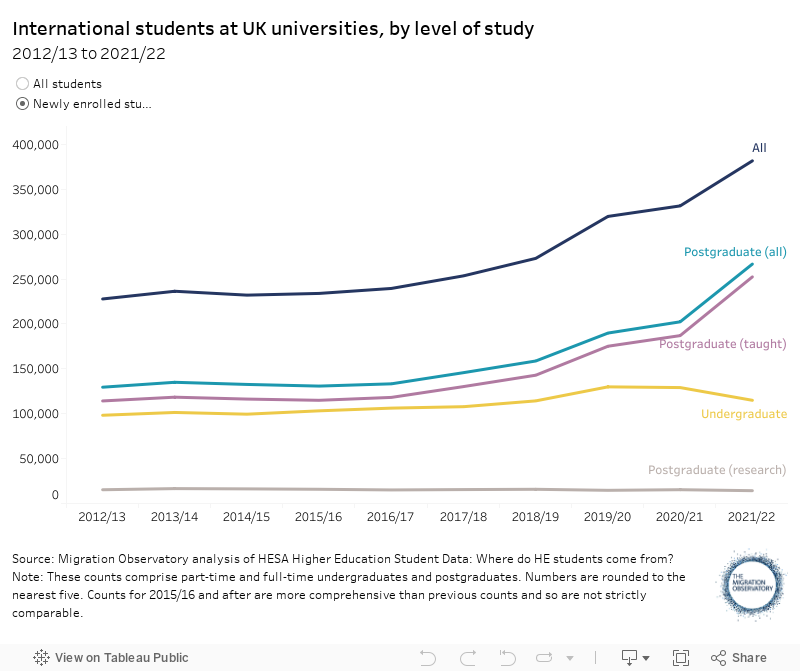

Most of the recent increase in international students was driven by those enrolling on master’s degrees and other taught postgraduate courses. The number of international students starting such courses increased by 77% between 2018/19 and 2021/22 (Figure 4). In the same period of time, the number of new undergraduate students from outside the UK remained unchanged, and the number of international students enrolling on a postgraduate research course declined by 10%.

Figure 4

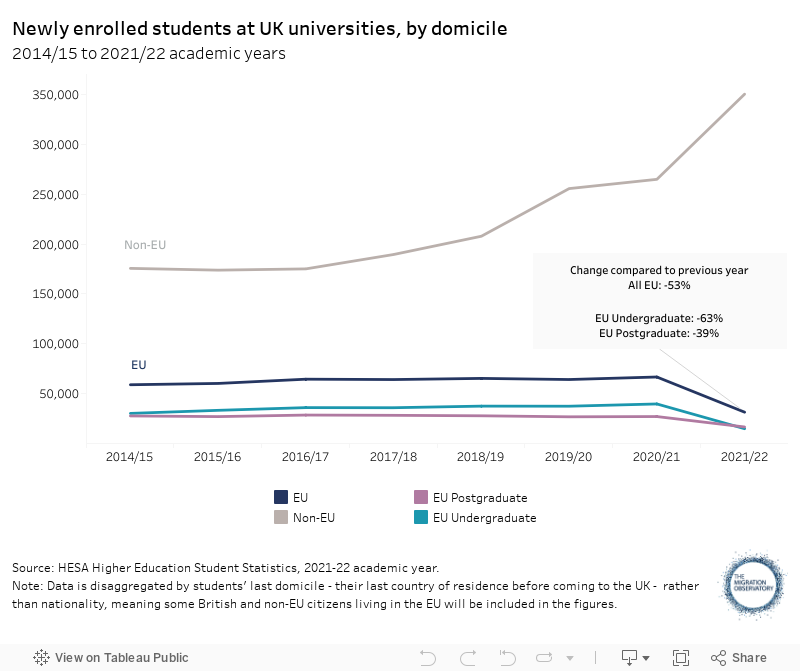

New student enrolments from the EU fell by 53% in the 2021/22 academic year, the first under post-Brexit rules

Student migration from the EU fell sharply in the 2021/22 academic year, the first under post-Brexit rules. There were 31,000 newly enrolled EU students, a fall of 53% compared to the previous year. The figure is in stark contrast to the number of new students from outside the EU, which grew by 32% over the same period.

As of the 2021/22 academic year, students from the EU are subject to the same rules as other international students, including the need to apply for a student visa, pay higher international fees, and cover their costs without access to government-backed loans. Undergraduate students have been particularly affected by the changes – enrolments from the EU fell by 63% in the 2021/22 academic year, compared to a decline of 39% among new postgraduate students (Figure 4).

Figure 5

In 2021/22, the top countries of origin for international students in the UK were China (26%), India (23%), and Nigeria (9%)

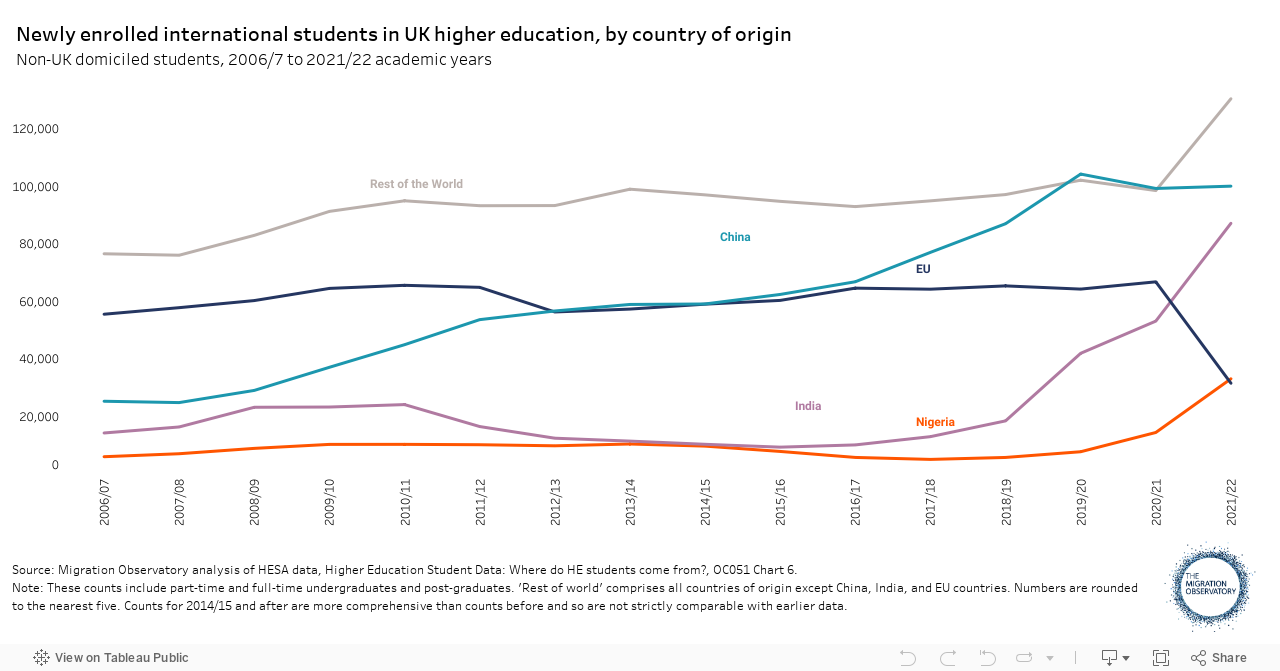

Most international students in the UK come from outside the EU – 92% in the 2021/22 academic year, compared to 73% five years before. In 2021/22, the top country of origin for new international students was China (100,000 students, 26% of the total), followed by India (87,000, 23%) and Nigeria (33,000, 9%).

From 2009/10 to 2019/20, UK universities increasingly relied on students from China, with their number growing by over 180% (Figure 6). By the 2019/20 academic year, Chinese students made up a third of all new international students, though this fell to 26% in 2021/22. Reliance on Chinese students is not unique to the UK. In 2021/22, they were also the top nationality among international students in the US, making up 31% of the total, and in Australia, with 21% of all foreign students.

Recently, much of the increase in international student numbers in the UK was driven by two countries of origin – India and Nigeria. Between 2018/19 and 2021/22, the number of students from these countries grew by 375% and 489%, respectively.

Indian student numbers declined from 2011/12 to 2018/19, possibly due to the closing of the post-study work visa route in 2011. As shown in Figure 9, Indian students are significantly more likely than others to work in Britain after graduation. In 2021, the government introduced a similar post-study work route, the Graduate Visa, which may have played some role in the recent increase in Indian and other international students. However, the reversal in Indian student numbers was already clear by 2019/20, before the policy change, and continued throughout the pandemic.

The number of Nigerian students rose sharply after 2020, following a period of decline. Research has found several likely explanations for this rise, including political and economic insecurity at home, relative ease of access to British universities, and the hope of obtaining work and settling in the UK long-term. As previously noted, Nigerian students are particularly likely to bring dependants to the UK (an average of 1.02 dependants per student in 2022, compared to 0.28 among all international students), which is consistent with plans to stay in the UK longer-term.

Figure 6

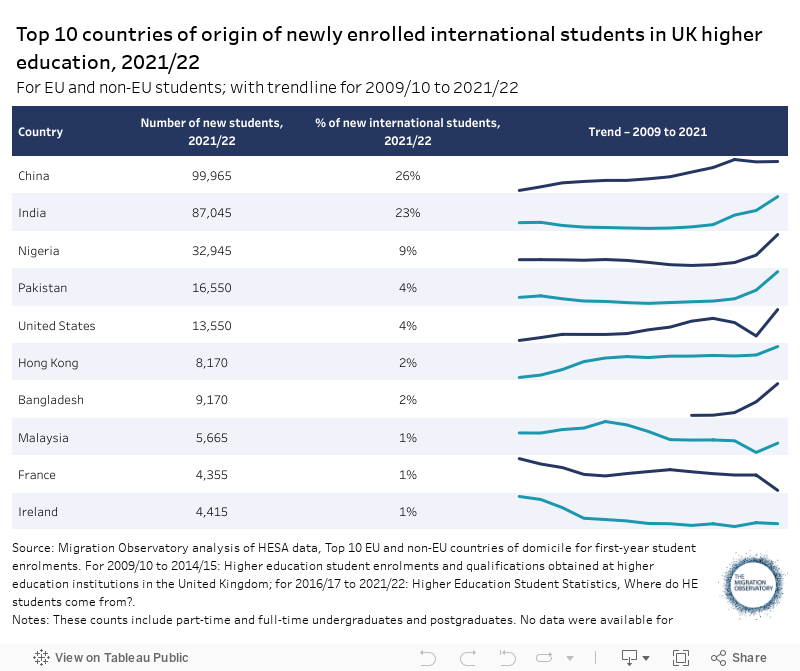

Table 1 shows the top 10 countries of origin for newly enrolled international students in UK higher education institutions in 2021/22. The number of students from several other countries, notably Pakistan and Bangladesh, has increased significantly in recent years. Meanwhile, the number of students from EU member states has fallen sharply.

Table 1

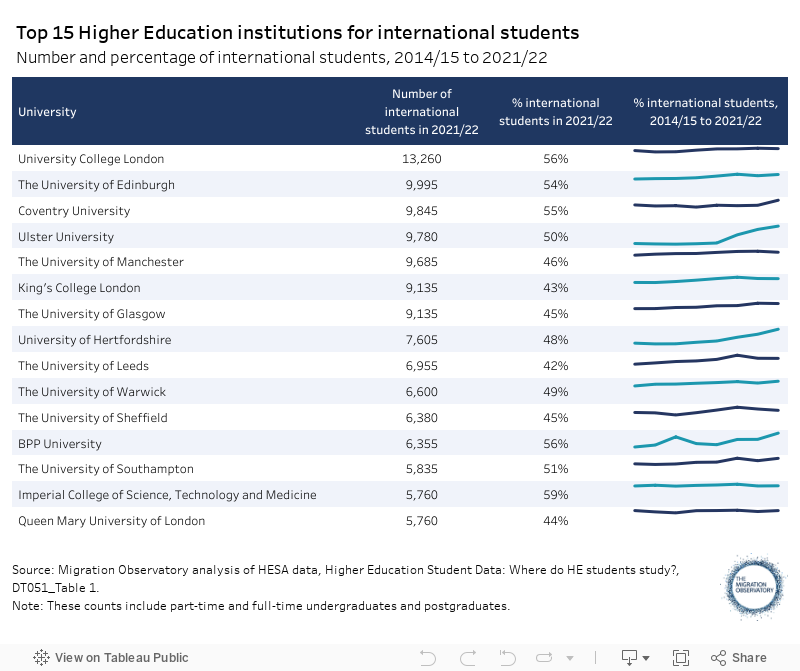

For the eighth year running, University College London received the largest number of new international students

For the eighth year in a row, the most popular UK university among international students moving to the UK was University College London, which received over 14,000 new international students, equivalent to 56% of its total intake. The London Business School (80%, or 1,165 international students) and the London School of Economics and Political Science (71%, or 5,295) were the institutions with the highest shares of international students.

Most universities in the top had a consistently high share of international students between 2014/15 and 2021/22 (Table 2). However, several institutions that were not traditional destinations for international students attracted rising numbers. For example, Ulster University in Northern Ireland became the 4th most popular destination for international students in the UK in 2021/22, with half of its intake coming from abroad. In 2014/15, the number of international students was almost eight times lower and only made up 11% of the total. Similar increases can be seen for the University of Hertfordshire (19% to 48%) and BPP University (21% to 56%).

The UK’s 24 Russell Group universities continue to attract a disproportionate share of the UK’s new international students. In 2021/22, they attracted 37% of newly enrolled international students, compared to 27% of all new students. However, the gap has narrowed recently as universities outside the Russell Group attract more international students. Their number at Russell Group institutions grew by 50% between 2014/15 and 2021/22, compared to 70% at other universities.

Table 2

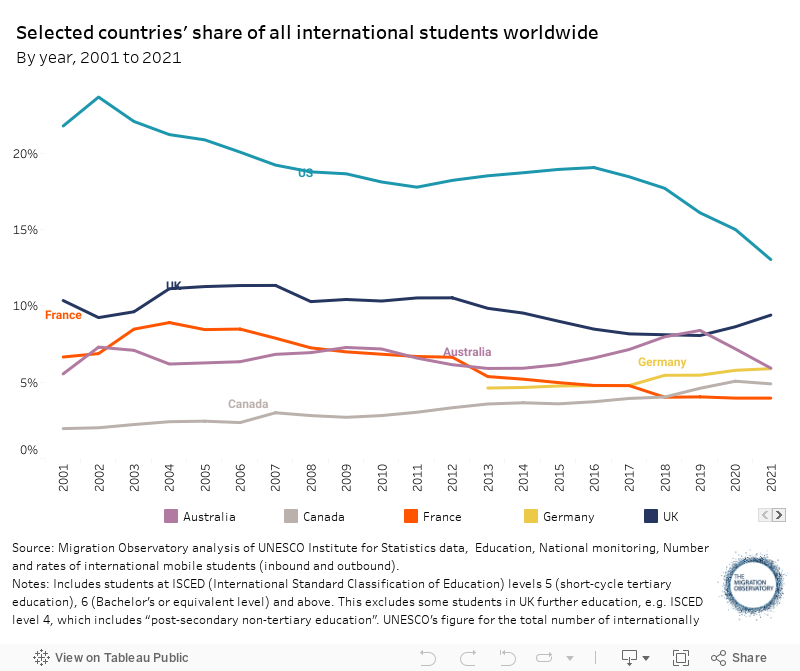

The UK recovered its position as the second most popular destination in the world for international students in 2021

The UK was the second most popular destination worldwide for international students in 2021, behind the United States. According to data from UNESCO, the UK had a 9% global market share, attracting around 600,000 tertiary students from around the world (this includes all those in higher education, as well as students on other post-secondary courses). By comparison, the US attracted around 833,000 international students in the same year, or 13% of the total. This marks a return to historical patterns after a brief period in 2018-19 when Australia approached and then surpassed the UK (Figure 7).

The UK lost global market share in international students between 2007 and 2019 despite increasing its absolute student numbers. This largely resulted from faster growth among other top destinations, including Australia and Canada, but also less traditional destinations, like China and New Zealand. The reversal of the trend since 2019 is likely due to several factors, including a rapid rise in the number of international students in the UK, as well as comparatively strict Covid and visa restrictions in countries such as the US and Australia, where international student numbers dropped between 2019 and 2021.

Changes in UK immigration policy, such as the closure of a post-study work route in 2012 and its subsequent reintroduction in 2021, may have also played a role. Research suggests that the UK’s immigration policies do influence students’ choices to study here, alongside a range of other factors, such as the exchange rate, economic growth in origin countries, and policies in competitor countries.

Figure 7

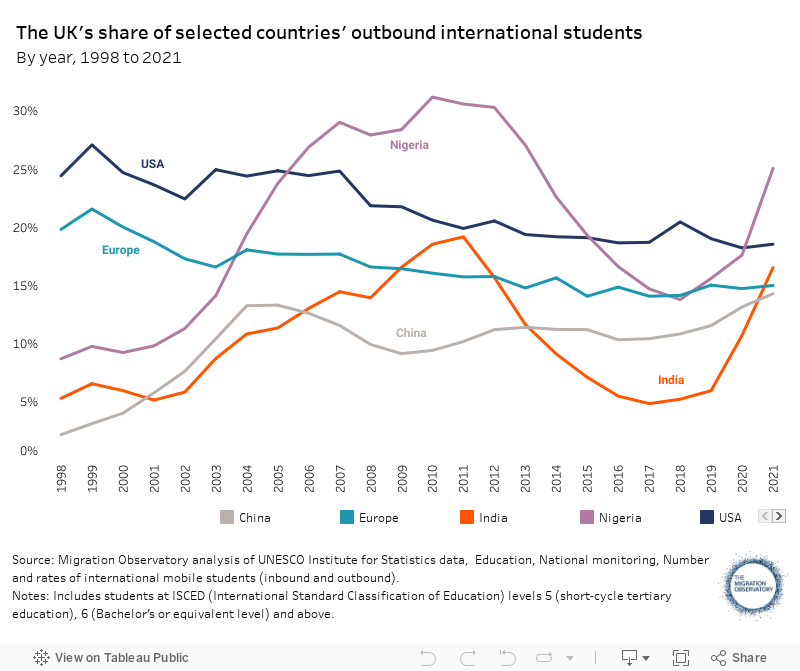

The UK’s recovery in its global market share of international students reflects its ability to attract an increasing proportion of students from India and Nigeria (Figure 8). From 2018 to 2021, the share of Indian students coming to the UK rose from 5% to 17%; among Nigerian students, the figure increased from 14% to 25%. The UK has also somewhat increased its share of Chinese international students, to 14% as of 2021. In contrast, the proportion of US and European students enrolled at British universities declined steadily after 2000.

Figure 8

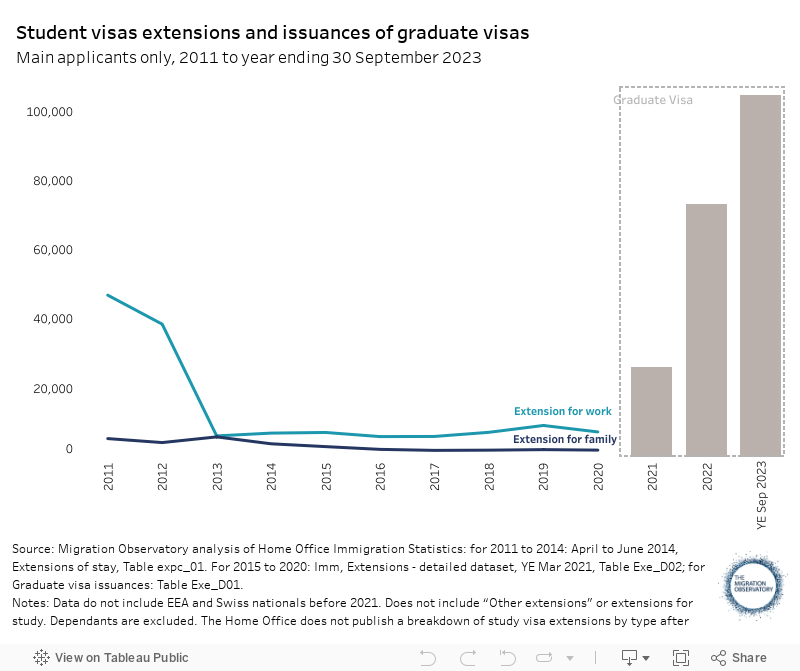

A record number of former students – almost 73,000 – extended their visas in 2022 through the new Graduate route

In 2022, almost 73,000 former students were issued a Graduate Visa, which allows them to live and work in the UK for two years after graduation or three years for PhD graduates. Introduced in July 2021, the new route saw high take-up and led to a large increase in the number of students extending their stay in the UK.

The number of students extending their stay in the UK through the Graduate route reached a record level in 2022 and continued to increase in 2023. In the year ending 30 September 2023, around 105,000 Graduate visas were granted to main applicants (Figure 9).

These numbers surpassed a previous peak of 55,000 total extensions in 2011, the year before the post-study work route was closed. From 2012 to 2020, non-EU students who wanted to stay in the UK after graduation generally had to switch to another type of visa, usually a work or family visa.

Some researchers argue that it benefits the UK economy when international students continue to work in the UK after graduating because they are often young, educated, and have specific skills such as language and cultural knowledge that can help British businesses break into new markets.

However, others argue that the UK benefits when international students return to their country of origin. This is because they may become ambassadors for the UK, enhancing the country’s soft power by becoming influential figures in their countries of origin. Returning students may also strengthen countries’ business and research links to the UK.

Figure 9

In the past, most non-EU students left the UK after their studies

Study visas are temporary and do not provide a direct route to settlement. This means that time spent on a study visa does not count towards the five years of residence in the UK that is ordinarily required before a migrant may apply for settlement.

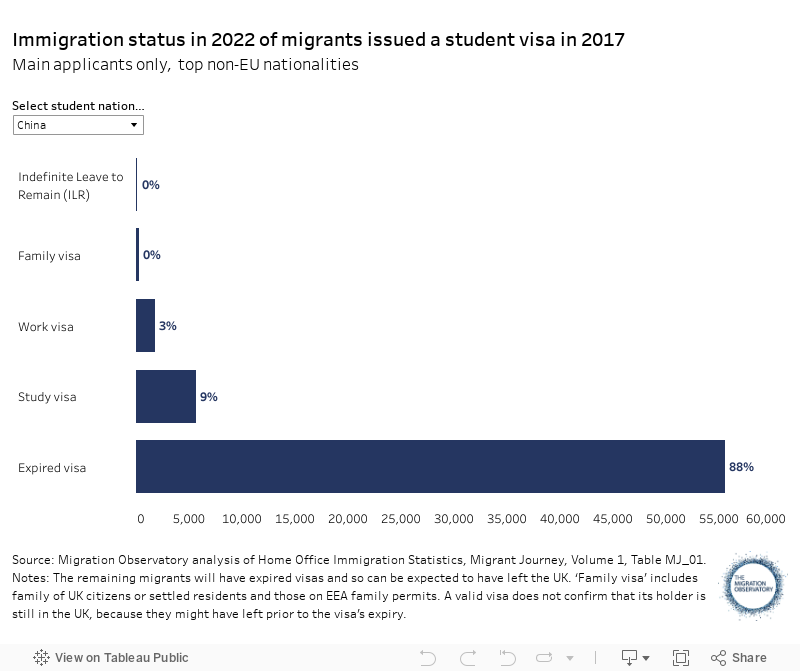

Among non-EU migrants issued an initial study visa in 2017, only 20% still had permission to stay in the UK (valid leave to remain) in 2022, around five years later. Approximately 8% (around 12,300) held work visas, another 9% (around 13,800) were still on study visas, and less than 0.1% (146) had indefinite leave to remain (Figure 10). The remaining 80% had an expired visa and would have been required to leave the UK. An overwhelming majority of these would have done so – Home Office data from 2020 showed that at least 98% of non-EU students with expired visas left the UK on time, which represents the minimum level of compliance (some people’s departures are not recorded, or are not matched against their arrival in the system).

There is some evidence that post-Covid cohorts of international students are staying in the UK longer than previous cohorts, however. It is too early to assess how this will affect the share of students who remain permanently, because much will depend on what share are able to secure long-term work visas. Nonetheless, it is possible that the share will increase in the coming years due to more work-motivated students coming to the UK.

There are notable differences between nationalities regarding their status five years after arriving in the UK on a study visa. For example, Indian students are more than five times as likely as Chinese students to have moved onto a work visa, while Chinese students are almost twice as likely as Indian ones to still have a study visa (Figure 10). Along with Indians, Nigerian and Pakistani students are also particularly likely to work in the UK after graduation.

Figure 10

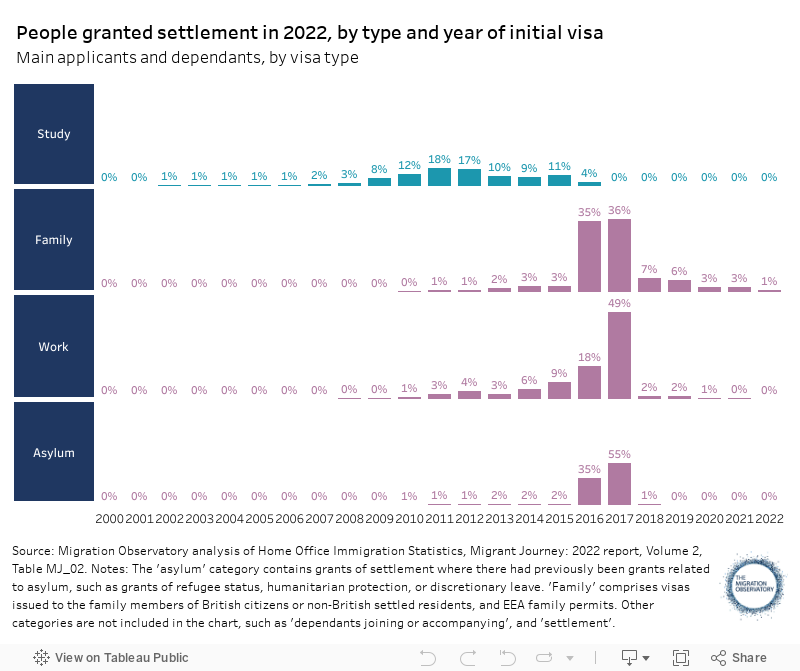

Students who remain in the UK usually take ten years to settle

Of all migrants granted settlement in 2022, 12% initially came to the UK on a study visa, and about two-thirds of this group arrived between 2010 and 2014, a period consistent with a roughly ten-year route to settlement (Figure 11).

The low number of students with settlement five years after arriving in the UK is due in part to students tending to be on a longer route to settlement than work, family, or asylum migrants – around ten years, rather than five years (for more detail, see the Migration Observatory briefing, Settlement in the UK).

Figure 11

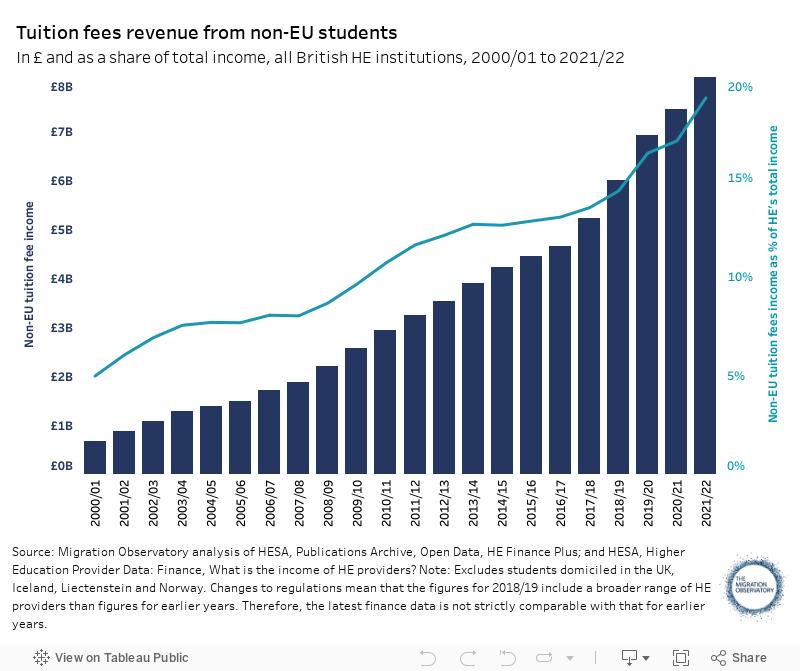

In 2021/22, more than a fifth of British universities’ total income came from the tuition fees of international students

British universities have become increasingly reliant on revenue from international students’ tuition fees. In the 2021/22 academic year, these fees amounted to approximately £10bn, or over 21% of British universities’ total income. Of these, a large majority came from non-EU students – around £8.9bn or 19% of the total. The share of income from non-EU students’ tuition fees rose sharply in the twenty years to 2021/22, from a little over 5% of the total (Figure 12).

Before Brexit, non-EU students paid higher fees than UK and EU students and thus generated significantly more revenue per person. Undergraduate fees in England for the latter were capped at £9,250 per year, whereas postgraduate tuition fees varied substantially, from £4,900 to over £30,000, with an average of around £11,000 per year. Starting in 2021/22, higher international fees apply to EU and non-EU students alike.

Researchers have shown that non-EU students have, in effect, been ‘cross-subsidising’ the education of domestic students – for example, by generating revenue for improved facilities or by sustaining a wider availability of courses. This has happened at a time of increasing fiscal strain for universities, particularly with regard to the costs of undergraduate teaching. Except for a minor increase in 2017, the tuition fee cap in England remained unchanged after reaching £9,000 a year in 2012. In real terms, however, its value fell to a little over £6,000 a year by 2023. A recent analysis by the Russell Group showed that, on average, UK universities faced a shortfall of £2,500 a year for each domestic undergraduate student.

Figure 12

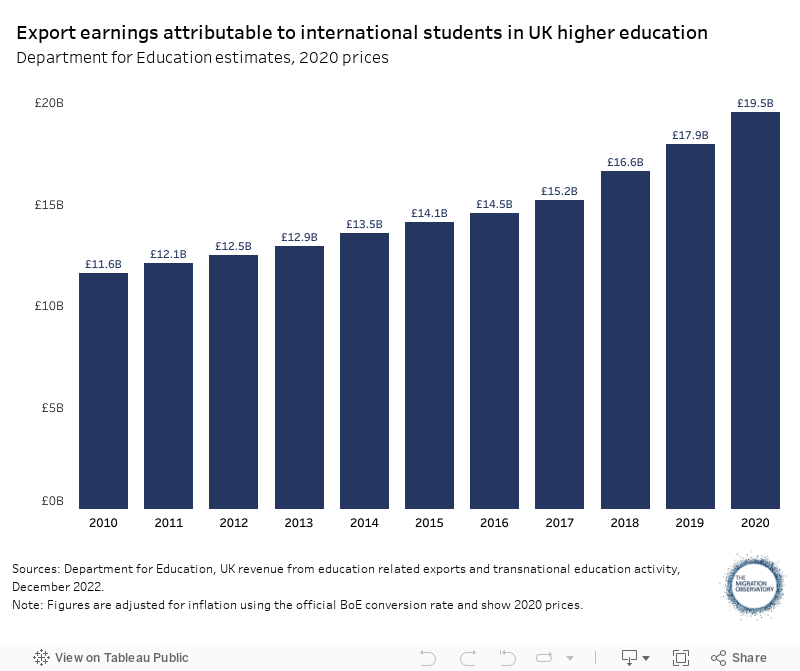

Research has consistently found that international students have a positive economic impact in the UK

The main economic impact of international students comes from the high tuition fees they pay, although there may be further contributions due to money they spend in the UK on accommodation, subsistence, and travel. One approach to quantifying this impact is to focus on export earnings from the higher education sector – expenditure on goods and services in the UK using money from abroad. According to the most recent estimates from the Department for Education, export earnings attributable to UK higher education reached £19.5bn in 2020 (Figure 13). In real terms, this marks an increase of 68% compared to the £11.6bn level seen in 2010. Estimates from other government departments and third-sector organisations broadly align with DfE figures. More broadly, a 2018 review by the Migration Advisory Committee found that the overall economic impacts of international students was positive.

After graduation, international students are expected to contribute to the UK economy by paying taxes. According to a government estimate, the introduction of the Graduate Visa route would result in £12.9bn of additional tax revenue – and £6.8bn of extra fiscal costs – for the Exchequer between 2021/22 and 2030/31. In other words, the fiscal costs of international students remaining in the UK are expected to be lower than the benefits. Note, however, that there is currently no data on the actual fiscal contributions of the most recent cohorts of international students who have participated in the Graduate Route in practice.

Figure 13

Evidence Gaps and Limitations

While good quality data exist on international students in higher education, mainly from the Higher Education Statistics Agency (HESA), there is comparatively little information on further education.

With regard to international students’ economic impact, the available research is limited largely to occasional studies of their export earnings: the revenue they generate through tuition fees and living expenditure. Yet international students may have broader effects that are difficult to measure, such as their contribution to research or the UK’s soft power.

Nor is much known about the economic activities of students while they are studying, such as how many work, and what kind of work they do.

Acknowledgements

With special thanks to Nick Hillman at HEPI, for his detailed feedback on several versions of this briefing. Research for this briefing was funded by Trust for London, which is one of the largest independent charitable foundations in London and supports work that tackles poverty and inequality in the capital. More details at www.trustforlondon.org.uk.

References

- Brown, R. (2009). Global horizons: How international graduates can help businesses. London: The Council for Industry and Higher Education.

- Conlon, G., Halterbeck, M. & Hedges, S. (2019). The UK’s tax revenues from international students post-graduation: Report for the Higher Education Policy Institute and Kaplan International Pathways. Oxford, UK: Higher Education Policy Institute.

- Conlon, G. P., Ladher, R., & Halterbeck, M. (2017). The determinants of international demand for UK higher education: Final report for the Higher Education Policy Institute and Kaplan International Pathways. Oxford, UK: Higher Education Policy Institute.

- Conlon, G., Litchfield, A., & Sadlier, G. (2011). Estimating the value to the UK of education exports. London, UK: Department for Business, Innovation and Skills, Research Paper 46.

- Department for Education (2018). UK revenue from education related exports and transnational education activity in 2015. London, UK: Department for Education.

- Department of Education, Skills and Employment (2022). International student monthly summary and data tables. Australian Government.

- Drayton, E. & Waltmann, B. (2020). Will universities need a bailout to survive the COVID-19 crisis? London, UK: Institute for Fiscal Studies.

- Halterbeck, M. & Conlon, G. (2021). The costs and benefits of international higher education students to the UK economy: Report for the Higher Education Policy Institute and Universities UK International. Oxford, UK: Higher Education Policy Institute.

- Hawthorne, L. (2008). The growing demand for students as skilled migrants. Washington, DC: Migration Policy Institute.

- HESA (2022a). The impact of the COVID-19 pandemic on 2020/21 Student data.

- HESA (2022b). What is the income of HE providers? Chart 1 and Table 6.

- Hillman, N. & Huxley, T. (2019). The soft-power benefits of educating the world’s leaders. HEPI Policy Note 16. Oxford, UK: Higher Education Policy Institute.

- Hillman, N. (2020). Covid-19 could be a curse for graduates but a boon for universities. London, UK: Times Higher Education.

- Hillman, N. (2020). From T to R revisited: Cross-subsidies from teaching to research after Augar and the 2.4% R&D target. HEPI Report 127. Oxford, UK: Higher Education Policy Institute.

- Hillman, N. (2022). 2022 HEPI Soft-Power Index: UK slips further behind the US for the fifth year running. Oxford, UK: Higher Education Policy Institute.

- Hill, C., & Beadle, S. (2014). The art of attraction: Soft power and the UK’s role in the world. London, UK: The British Academy.

- Holden, J., & Tryhorn, C. (2013). Influence and attraction: Culture and the race for soft power in the 21st century. London, UK: British Council.

- House of Lords (2014). Select committee on soft power and the UK’s influence, report of session 2013–14: Persuasion and power in the modern world. London, UK: The Stationery Office Limited.

- Home Office (2020a). Fifth report on statistics relating to exit checks. London, UK: Home Office.

- Home Office (2022a). Immigration statistics quarterly release, year ending June 2022, Study sponsorship (Confirmation of acceptance for Studies) – CAS_D02. London, UK: Home Office.

- Home Office (2022b). Migrant journey: 2021 report. London, UK: Home Office.

- IIE (2022). Open Doors, Data, International Students, Enrollment Trends, Top Ten Places of Origin for International Students.

- Johnson, J., Adams, J., Ilieva, J., Grant, J., Northend, J., Sreenan, N., Moxham-Hall, V., Greene, K. & Mishra, S. (2021). The China question: Managing risks and maximising benefits from partnership in higher education and research. London, UK: The Policy Institute, King’s College London.

- Kelly, U., McNicoll, I., & White, J. (2014). The impact of universities on the UK economy. London, UK: Universities UK.

- Lomer, S. (2017). Recruiting international students in higher education: Representations and rationales in British policy. London, UK: Palgrave Macmillan.

- London Economics (2018). The costs and benefits of international students by parliamentary constituency: Report for the Higher Education Policy Institute and Kaplan International Pathways. London: London Economics.

- Mellors-Bourne, R., Humphrey, C., Kemp, N., & Woodfield, S. (2013). The wider benefits of international higher education in the UK. London, UK: Careers Research & Advisory Centre (CRAC) Ltd for the Department for Business, Innovation and Skills, BIS Research Paper 128.

- Migration Advisory Committee (2018). Impact of international students in the UK. London, UK: Migration Advisory Committee.

- Office for National Statistics (2020). Population of the UK by country of birth and nationality.

- ONS. (2021). Using statistical modelling to estimate UK international migration. Newport: ONS.

- Prazeres, L., & Findlay, A. (2017). An audit of international student mobility to the UK. Southampton, UK: ESRC Centre for Population Change, Working Paper 82.

- QS (2019). International student survey 2019. London, UK: QS.

- UCAS (2022). Postgraduate fees and funding. Accessed 26 July 2022.

- UNESCO Institute for Statistics. (2012). International standard classification of education: ISCED 2011. Montreal: UNESCO Institute for Statistics.

Related material

- Migration Observatory briefing – Election 2015 Briefing – Why do International Migrants Come to the UK?

- Migration Observatory briefing – Immigration by Category: Workers, Students, Family Members, Asylum Applicants

- Migration Observatory briefing – Migrants in the UK: An Overview

- Migration Observatory briefing – Settlement in the UK